4 things to know regarding your auto insurance premium, according to insuranceQuotes

JUN 14, 2017 | BY DENNY JACOB, PROPERTYCASUALTY360

A moving violation can affect your premium for three to five years, so here’s what drivers should ask their insurance agents. (Photo: Shutterstock)

A moving violation ticket will leave a bitter taste in any driver’s mouth.

They will spike a driver’s auto insurance premium, and many come with hefty financial penalties. But depending on the violation or which state the driver is located, it could be an extremely burdensome on a driver’s wallet.

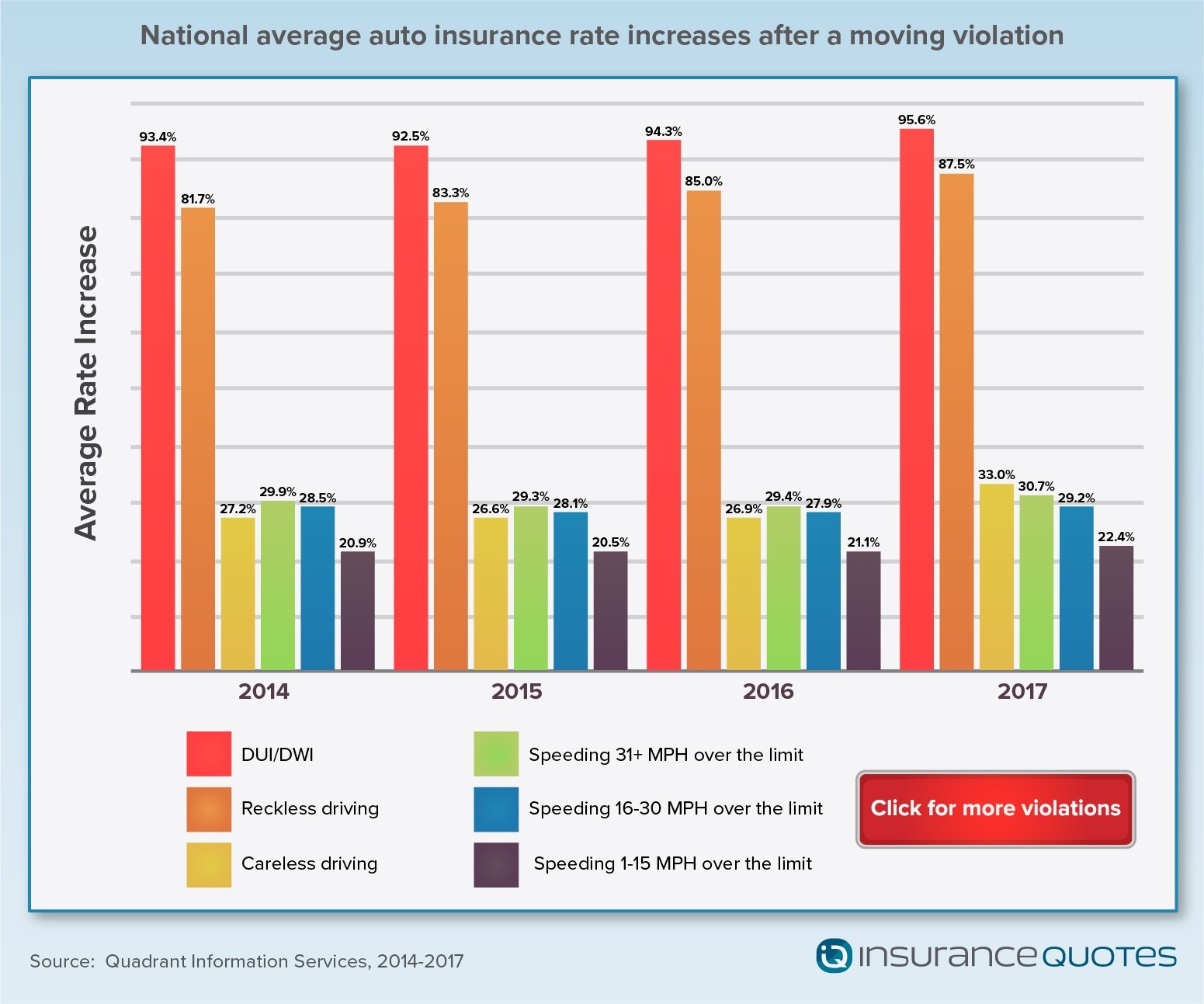

For the fourth consecutive year, insuranceQuotes commissioned a Quadrant Information Services study that found car insurance premiums can climb by as much as 96% after a single moving violation on average nationwide.

The study analyzed the average national premium increase for one moving violation in 21 different categories, including careless driving, reckless driving, driving under the influence and speeding. As in years past, the study found the economic impact on one’s insurance premium varies significantly among different types of violations and among different states.

Here are some of the study’s key findings along with some advice on what you can do after a moving violation to keep your rates as low as possible:

DUI/DWI produce the highest rate increases over the last four years while speeding 1-15 miles per hour over the limit produce the lowest rate increase. (Photo: insuranceQuotes)

Your premium increase will depend on the specific violation.

Take, for instance, the difference between reckless and careless driving.

According to Robert Nevo, a former Georgia police officer and current owner of Nevo Driving Academy, careless driving is usually defined as “a minor lapse in judgment,” such as following too closely to the vehicle in front of you. Reckless driving, however, concerns more “intentional acts,” such as driving in a way that shows no regard for the safety of others.

“Moving violations are typically weighted with a point system. This makes an excessive speeding violation much more severe than, say, a broken taillight violation,” said Nevo. “Insurance companies often see more points against a driver’s license as an increased risk. Therefore, you’re going to see higher premiums for that driver.”

Across the country, premium increases are directly affected by where the driver lives. (Photo: Shutterstock)

Your premium increase could be expensive.

Whether it’s a minor or major offense, your wallet will feel the toll.

According to the National Association of Insurance Commissioners (NAIC), the average annual U.S. auto insurance premium is $866. That means an 88% premium spike for one reckless driving offense will result in an increase of just more than $750 per year.

Even relatively “minor” infractions, such as following too close or not yielding to a pedestrian, can mean paying an average of $260 more per year for car insurance. Driving under the influence carries an expensive insurance penalty, with a single infraction resulting in an average premium spike of $1,086.

Across the 50 states, depending on the moving violation, premiums can increase by high percentages or very little. (Photo: Shutterstock)

It all depends on the state.

The impact on your auto insurance premium largely depends on where you live.

For instance, a first-time DUI conviction in North Carolina will result in an average premium increase of 298% (in Hawaii it’s 209%, 187% in California, and 165% in Michigan). Meanwhile, the same violation in Maryland will only result in an average premium increase of 21%.

Perhaps the starkest difference can be seen in a violation for failure to wear a seatbelt.

In North Carolina, just one ticket for this infraction will result in an average premium increase of 27% (22% in Oregon and 20% in Utah). Meanwhile, in 32 states this particular violation moves the premium needle by less than 5%, including seven states where it has no impact on the premium price at all.

While a moving violating will affect your premium, there are options drivers can discuss with insurance agents to save money. (Photo: Shutterstock)

You can still save money.

While your premium will be impacted for quite some time, the moving violation will eventually be erased from your driving record. How long you’ll feel the increased premium’s impact depends on the severity of the violation as well as the individual state laws. Here are some tips for the bumpy times ahead.

Seek forgiveness: If this your first moving violation, especially a minor one such as a failure to signal, talk to your auto insurer. They’re typically going to be somewhat forgiving for a small infraction. Take advantage of any driving classes your state might be offering to remove one or two moving violations from your record.

Make a deal: If your violation isn’t too severe, look for a plea bargain when your day at traffic court is due.

Shop around: Shopping for a new car insurance policy after receiving a traffic moving violation may also be a good idea, though it’s unlikely you’ll be able to hide the violation altogether.

Wait it out: Eventually, your driving record will go back to its original clean slate, but that could take anywhere between three to five years.