A Highway 14 overpass that collapsed onto Interstate 5 in the San Fernando Valley section of Los Angeles in 1994

SAN DIEGO — An earthquake fault running from San Diego Bay to Los Angeles is capable of producing a magnitude-7.4 earthquake that could affect some of the region’s most densely populated areas, according to a study released Tuesday.

The study looked at the Newport-Inglewood and Rose Canyon systems — previously thought to be separate — and concluded they actually form a continuous fault that runs underwater from San Diego Bay to Seal Beach in Orange County and on land through the Los Angeles basin.

The fault poses a significant hazard to coastal Southern California and Tijuana, Mexico, according to the study. It could produce up to a magnitude-7.3 quake if the offshore segments rupture and a magnitude-7.4 quake if the onshore segment also ruptures, according to the study by Scripps Institution of Oceanography at the University of California San Diego.

Even a moderate quake on the fault could have a major impact on the region, according to Valerie Sahakian, the study’s lead author. “This system is mostly offshore but never more than four miles from the San Diego, Orange County, and Los Angeles County coast,” Sahakian was quoted as saying in a press release from the American Geophysical Union.

The fault’s most recent major rupture occurred in 1933 in Long Beach and produced a magnitude-6.4 earthquake that killed 115 people.

The study looked at data from previous and new seismic surveys that included sonar studies of the offshore fault. Researchers looked at four segments of the fault that were offset — known as stepovers — and found the disconnections weren’t wide enough to prevent the entire offshore section of the fault from rupturing.

Researchers also looked at the onshore segment of the fault and concluded that there have been three to five ruptures in the past 11,000 years along the northern section and one quake about 400 years ago at the southern end.

Researchers at the Nevada Seismological Laboratory assisted with the study, which was funded by Southern California Edison. It was accepted for publication in the American Geophysical Union’s Journal of Geophysical Research.

4 things to know regarding your auto insurance premium, according to insuranceQuotes

JUN 14, 2017 | BY DENNY JACOB, PROPERTYCASUALTY360

A moving violation can affect your premium for three to five years, so here’s what drivers should ask their insurance agents. (Photo: Shutterstock)

A moving violation ticket will leave a bitter taste in any driver’s mouth.

They will spike a driver’s auto insurance premium, and many come with hefty financial penalties. But depending on the violation or which state the driver is located, it could be an extremely burdensome on a driver’s wallet.

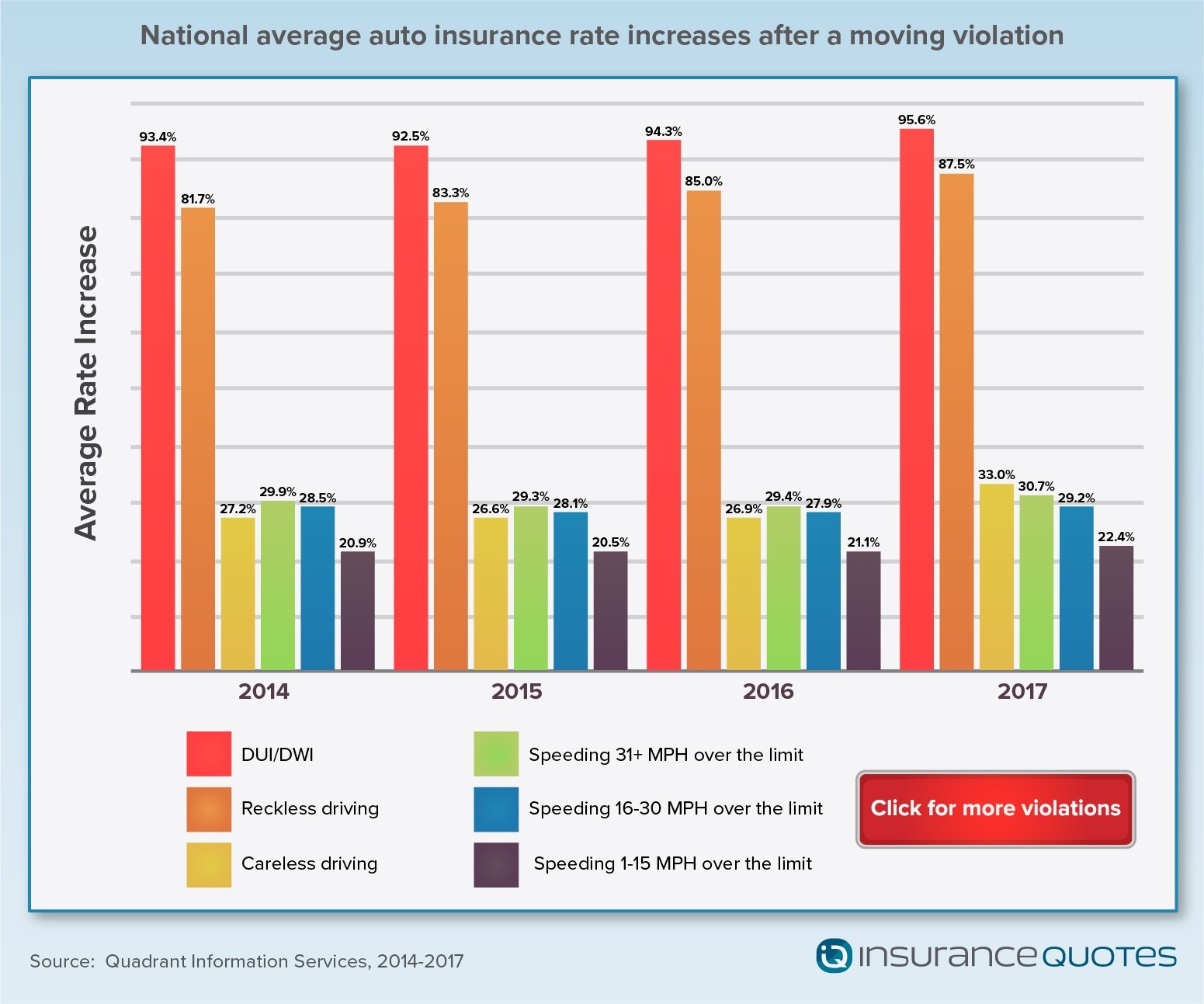

For the fourth consecutive year, insuranceQuotes commissioned a Quadrant Information Services study that found car insurance premiums can climb by as much as 96% after a single moving violation on average nationwide.

The study analyzed the average national premium increase for one moving violation in 21 different categories, including careless driving, reckless driving, driving under the influence and speeding. As in years past, the study found the economic impact on one’s insurance premium varies significantly among different types of violations and among different states.

Here are some of the study’s key findings along with some advice on what you can do after a moving violation to keep your rates as low as possible:

National average auto insurance rate increases after a moving violation

DUI/DWI produce the highest rate increases over the last four years while speeding 1-15 miles per hour over the limit produce the lowest rate increase. (Photo: insuranceQuotes)

Your premium increase will depend on the specific violation.

Take, for instance, the difference between reckless and careless driving.

According to Robert Nevo, a former Georgia police officer and current owner of Nevo Driving Academy, careless driving is usually defined as “a minor lapse in judgment,” such as following too closely to the vehicle in front of you. Reckless driving, however, concerns more “intentional acts,” such as driving in a way that shows no regard for the safety of others.

“Moving violations are typically weighted with a point system. This makes an excessive speeding violation much more severe than, say, a broken taillight violation,” said Nevo. “Insurance companies often see more points against a driver’s license as an increased risk. Therefore, you’re going to see higher premiums for that driver.”

Across the country, premium increases are directly affected by where the driver lives. (Photo: Shutterstock)

Your premium increase could be expensive.

Whether it’s a minor or major offense, your wallet will feel the toll.

According to the National Association of Insurance Commissioners (NAIC), the average annual U.S. auto insurance premium is $866. That means an 88% premium spike for one reckless driving offense will result in an increase of just more than $750 per year.

Even relatively “minor” infractions, such as following too close or not yielding to a pedestrian, can mean paying an average of $260 more per year for car insurance. Driving under the influence carries an expensive insurance penalty, with a single infraction resulting in an average premium spike of $1,086.

Across the 50 states, depending on the moving violation, premiums can increase by high percentages or very little. (Photo: Shutterstock)

It all depends on the state.

The impact on your auto insurance premium largely depends on where you live.

For instance, a first-time DUI conviction in North Carolina will result in an average premium increase of 298% (in Hawaii it’s 209%, 187% in California, and 165% in Michigan). Meanwhile, the same violation in Maryland will only result in an average premium increase of 21%.

Perhaps the starkest difference can be seen in a violation for failure to wear a seatbelt.

In North Carolina, just one ticket for this infraction will result in an average premium increase of 27% (22% in Oregon and 20% in Utah). Meanwhile, in 32 states this particular violation moves the premium needle by less than 5%, including seven states where it has no impact on the premium price at all.

While a moving violating will affect your premium, there are options drivers can discuss with insurance agents to save money. (Photo: Shutterstock)

You can still save money.

While your premium will be impacted for quite some time, the moving violation will eventually be erased from your driving record. How long you’ll feel the increased premium’s impact depends on the severity of the violation as well as the individual state laws. Here are some tips for the bumpy times ahead.

Seek forgiveness: If this your first moving violation, especially a minor one such as a failure to signal, talk to your auto insurer. They’re typically going to be somewhat forgiving for a small infraction. Take advantage of any driving classes your state might be offering to remove one or two moving violations from your record.

Make a deal: If your violation isn’t too severe, look for a plea bargain when your day at traffic court is due.

Shop around: Shopping for a new car insurance policy after receiving a traffic moving violation may also be a good idea, though it’s unlikely you’ll be able to hide the violation altogether.

Wait it out: Eventually, your driving record will go back to its original clean slate, but that could take anywhere between three to five years.

The origin of a water leak is frequently a determining factor in whether or not the resulting damage will be covered by a standard homeowners policy. (Photo: Shutterstock)

Home water damage comes from many different sources, is classified in different ways, and falls under different areas of coverage.

For instance, natural flooding is considered to be very different from standard water damage and is covered under separate policies. When you’re confronted with a claim, here are some of the things you need to look for to judge the matter correctly according to the policy.

Gradual vs. sudden damage

This is by far the most important distinction. Homeowners insurance is meant to cover sudden unexpected damage to a home. The trouble with water damage is that it can hide for quite a long time before it becomes apparent. This leads to conflicts about whether or not the original cause of the damage was gradual or sudden.

For instance, discovering a crack in a foundation might be a cause for a claim. But if the crack wasn’t found and water seeps into the basement and causes damage that might not be covered because it was gradual. Another example is a slow faucet leak under a sink. If the cabinet floor underneath the sink gets damaged, that’s gradual.

Determining the fate of soft contents after a catastrophe involves more than an educated guess.

Examples of sudden damage include a pipe breaking in a freeze that leads to a huge flood, or a tree poking a hole into the roof of a home after falling and letting storm water in. But these can also lead to secondary damage that doesn’t show up till much later, which can create conflicts with policyholders.

If the smashed roof was repaired, but soaked insulation wasn’t remedied, mold could develop and lead to another claim. A common example is a sudden failure of an appliance. A washer in a dishwasher might gradually fail, but once it does the damage can be sudden.

Policy will be the guide

The policy will be the guide about whether or not this secondary damage can be covered or not. For instance, some states require insurance companies to cover secondary mold damage due to a legitimate water damage claim. It’s up to adjusters to know the exceptions and to understand exactly what the policy covers.

Adjusters have to get a clear idea of where the water came from and why before adjusting a claim. (Photo: Shutterstock)

Water damage vs. flooding

Most homeowners policies will cover sudden water damage except in one major case, flooding. Flooding is not covered by most homeowner’s policies. It requires separate flood insurance. So, how is flooding defined?

In the most general sense, once water from a natural source (e.g., a river or the sky) touches the ground, it is then considered flood water. Your insurance company may put in other restrictions, but this is the core difference. This is why storm water falling in from a hole in the roof is covered by some policies, but a swollen river washing away a porch is not.

However, most homeowners are not conversant with this difference. It is common to say that a room is flooded when there is water all over the floor, and this can set off alarm bells for insurance adjusters. Adjusters have to get a clear idea of where the water came from and why before adjusting a claim. Too many simply hear the word flood and automatically deny it.

How to make a judgment

Deciding which category a claim falls into is tricky, but acquiring evidence is the same as any other claim. Ask for home maintenance records, photos, and descriptions of what the homeowner did before and after the incident.

Interview any professionals including water damage professionals who worked on the situation prior to your examination. Ask if any cleanup work was done and what preventative measures the policyholder took to prevent further damage. From there, it’s just a matter of using your expertise and the wording of the policy to know whether or not the claim is covered.

Michael Jacobs is the head of the public relations department at ServiceProsLocal.com, with a primary focus on customer satisfaction. He focuses on water damage restoration, environmental friendly house building and plant cultivation. Contact him at michael@serviceproslocal.com.

The American Red Cross recommends that senior citizens create a personal support network made up of several individuals who will check in on you in an emergency, to ensure your wellness and to give assistance if needed. This network can consist of friends, roommates, family members, relatives, personal attendants, co-workers and neighbors. Ideally, a minimum of three people can be identified at each location where you regularly spend time, for example at work, home, school or volunteer site.

There are seven important items to discuss and implement with a personal support network:

Make arrangements, prior to an emergency, for your support network to immediately check on you after a disaster and, if needed, offer assistance.

Exchange important keys.

Show them where you keep emergency supplies.

Share copies of your relevant emergency documents, evacuation plans and emergency health information card.

Agree on and practice methods for contacting each other in an emergency. Do not count on the telephones working.

You and your personal support network should always notify each other when you are going out of town and when you will return.

The relationship should be mutual. You have a lot to contribute! Learn about each other’s needs and how to help each other in an emergency. You might take responsibility for food supplies and preparation, organizing neighborhood watch meetings and interpreting, among other things.

Shopping around for a new or new-to-you used car can be exciting. But before you step on the lot, be mindful of a few sales tactics and how to ensure you stay in control. Doing some homework ahead of time can help you buy in confidence.

Mixed Negotiations

Also known as the “four square” method, this sales tactic combines multiple, unrelated factors into a single transaction. The sales manager writes the price of the car, the down payment, trade-in value and the desired monthly payment into four boxes. If you want a certain trade-in price or a set monthly payment, other numbers may increase to compensate.

How to prepare: Shop your trade-in around multiple dealerships to get an estimate of its true value, and know not to negotiate based on your desired monthly payment.1

Inflated Interest Rates

Some car dealerships may advertise a certain interest rate, then make a last-minute change to financing.1

How to prepare: Secure a car loan through a bank or other outside party and come to the dealership with pre-approval in hand. Know your credit score beforehand so you’re confident about what you can afford, and triple-check all numbers in your paperwork.2

Spot Delivery

Some car buyers have driven a car off the lot without securing financing. This means that a few weeks later, the car dealership could call to say the loan application was rejected and that they need new paperwork—with a higher interest rate or down payment.

How to prepare: Never sign a deal or drive away in your new car if you don’t see your interest rate written down.3

Data breaches seem to be happening more and more often, with data thieves targeting both small companies and global giants.1 Data thieves are always on the lookout—and you should be too. Here’s what you need to know about protecting yourself from data breaches.

How Hacks Can Happen

Technology seems to offer the promise of keeping us safer—so what can lead to hacks? It’s a complicated issue, including:

Multiple entry points. People and companies access data from multiple places, including desktop computers, phones and tablets. These are all potential entry points for hackers, making it more complicated to protect against a data breach.

High volume of malicious activity. Nearly 1 million pieces of malicious software are published each day,2 making it difficult to guard against every new threat.

How you Can Help Protect Yourself

Whether or not there have been reports of a data breach, you should always do everything you can to keep your information secure. Here are some tips to consider:

Create complex passwords. Use different ones for each account, and change your passwords3if a company you’ve recently interacted with gets hacked.

Shop with a credit card. You may have less liability for fraudulent credit card charges,4 but you may be responsible for more than $500 in charges if your debit account is hacked.5

Watch for fraud. If you receive a notice about the data breach, call the company to confirm that it is legitimate.

Guard against identity theft. One in three people who experience a data breach will become an identity theft victim, according to Javelin Strategy & Research.6 If you are one of them, contact each credit card company to set up fraud alerts and freeze your accounts. Then get in touch with your local Social Security office for next steps.

Set up account alerts. You may be able to receive notifications of suspicious purchases or those that exceed a certain dollar amount. This may give you a heads-up that you’ve been hacked.

Disclaimer: Farmers and Mike Guiffrida are not responsible for, and does not endorse or approve, either implicitly or explicitly, the content of any third party sites hyperlinked from this page. We have no discretion to alter, update, or control the content on the hyperlinked, third party site. Access to third party sites is at the user’s own risk, is being provided for informational purposes only and is not a solicitation to buy or sell any of the products which may be referenced on such third party sites.

If you get a ticket, that is, a moving violation, make sure you go to Traffic School! If you have no prior tickets in the last 18 months, it will save you lots of money on rate increases and will expunge the ticket from your record.

Talk to Mike about the increase in your rates if you have just one ticket!

As you are most likely aware, the National Weather Service is anticipating that the El Nino Conditions will bring heavy rains to Southern California this winter. Nobody truly knows what is going to happen but we want you to know that we are preparing for the worst so we can best help you and your insureds when they need it the most. We pride ourselves on having one of the largest and most responsive and experienced fleets in the industry. However, expectations need to be adjusted in the event that we get several large storms and demand for our services are high.

I can tell you based on previous El Nino years that no single restoration company will be able to handle the demand if we get the type of rain storms that are being predicted. Our standard one hour response time will have to be extended and prioritized based on severity. This is a similar approach that most insurance claims departments take in these conditions. Unfortunately, we also won’t be able to offer free estimates during this period. We regret this but we but we are still able to give free advice and help your policyholders anyway we can regardless of whether the damage is a covered loss or not.

In addition, the anticipated storms may create other difficult situations that we would like you to be aware of. Aside from the potential for delayed response times, your policyholders may encounter coverage issues due to flooding. It is also important to remember that we often can’t start the dry out process until the rain stops. This is especially true if the water is coming through an exterior wall from the ground or through a leaking roof. Also, please keep in mind that roofers will be equally busy during this period.

We are recommending to all agents to do their best to provide their policyholders with tips ahead of time and to have them clean out gutters, repair roofs, check drains, and get sand bags before they absolutely need them. This may help minimize the number and severity of claims due to the El Nino conditions. We would like to thank you so much for your confidence and continued business through the years. At ServiceMaster by Rapid Response, we believe that this El Nino season may be another challenge that we can help your policyholders manage.

Sabrina at Servicemaster by Rapid Response

sabrinazimmerman@smrapid.com

Insurance fraud is not simply the act of people taking advantage of a faceless corporation, as the ethically challenged may claim. It costs all Americans through increased premiums, and it can take a much worse toll in some cases – even potentially resulting in death.

Auto Insurance Fraud Is on the Rise

According to the National Insurance Crime Bureau (NICB), auto insurance is the greatest component of overall insurance fraud. In the 2013 NICB report, suspected cases of auto insurance fraud rose 12.7% from 2011 to 2012, reaching a nationwide total of 78,024. This raised the three-year total from 2010 to 2012 to over 209,000 questionable claims (QCs).

To put this in perspective, auto-related QCs during 2012 were over four and a half times more prevalent than the next highest category (17,183 homeowner’s personal property QCs) and almost seventeen and a half times more than the third place category (workers compensation, including employer’s liability).

Studies estimate almost 25% of the bodily injury claims related to auto crashes are bogus. Property and casualty claims against auto insurance are not much better, coming in at around a 10% fraud rate.

The NICB estimates the direct cost to you at around $200-$300 per year extra tacked onto your premium. The indirect costs are likely to be far more than that, estimated at around $1,000 per family according to the Texas Department of Insurance.

The indirect costs are not always obvious, but they are significant. For example, some portion of the prices you pay for goods and services is devoted to covering the inflated insurance costs of the business – and for fraud schemes, businesses are even more tempting targets than individuals.

Estimates vary on the overall cost, but the Coalition Against Insurance Fraud puts the cost of fraudulent claims in the range of $80 billion annually. Claims tend to rise during difficult economic times, and the recent recession was no different.

Types of Fraudulent Claims

What is the nature of all of these bogus claims? Auto insurance fraud is typically broken into two classifications – “hard” and “soft”.

Hard fraud occurs when an insurable event is either staged or fabricated outright. This includes scams such as phony hit and run accidents, triggered rear-end collisions, and fake car thefts.

Soft fraud refers to inflating a legitimate claim to cover nonexistent or unrelated charges. Examples include claiming damage from a previous event or racking up unjustified medical expenses claiming the wreck was at fault. Underwriting fraud, or misrepresenting your insurance information to lower your premiums, may also be considered a form of soft fraud.

The Auxiliary Dangers

In the case of auto insurance fraud, hard fraud is on a significant increase and staged accidents account for the greatest part of it. Staged accidents often involve innocent people who happen to be in the wrong place at the wrong time and get inadvertently caught up in a staged collision or a subsequent chain reaction.

There have been multiple cases of injuries and deaths from staged accidents that spiral out of control, and people have been successfully prosecuted as a result. Unfortunately, that does not bring back the deceased or heal the disabled.

Help Stop Auto Insurance Fraud

If you suspect auto insurance fraud, or any other type of insurance fraud, the has a toll-free hotline (1-800-835-6422 or 1-800 TEL-NICB) that you can call to report the fraud anonymously for further investigation. We hope that you never find yourself in this situation – but if you do, please be part of the solution and not part of the problem.

1 in 3 pets will need unexpected veterinary care this year.

4 out of 5 pets will experience a medical emergency in their lifetime

Annual medical costs for a pet range between $500 to $1000 and dramatically increase to $8000+ for severe illnesses such as cancer treatment.

We predict close to half of our customers own a pet, however, most owners are uninsured and unaware that affording the best care for their pet is now no longer a concern.

Pet Insurance offered by Pets Best provides comprehensive insurance for routine medical checkups, accidents and serious illnesses for an average annual rate of $425.

Plans offer comprehensive coverage for accidents and illnesses

Treatment Savings for Pet Owner

Cancer, $6,000+

Broken leg, $3,000+

Swallow foreign body / choking, $1,700

Routine, $500 –

medical checkups (e.g. vaccinations, teeth cleaning), $1,000

Optional coverage for routine/wellness care

There are no upper age limits.

Pets Best does not require medical records or a vet exam to enroll.

Pets Best policies also cover unexpected out-of-pocket expenses for pets related to emergency visits, behavioral conditions, surgeries, hereditary conditions, international travel and more.

Does pet insurance cover when a pet dies?

No. Pet insurance through Pets Best covers the ongoing health of the pet. Currently in certain states there is a liability coverage in home and auto that covers pet related accidents or death up to $500. However, pet insurance is different and covers the ongoing health of the pet.

Is pet insurance worth the cost?

$35/month gets you:

Historically, people have been confused about what pet insurance covers due to complicated terms and conditions. Farmers’ partnership with Pets Best is simple and transparent and allows pet parents to enjoy great benefits, like:

Choose any licensed veterinarian or specialist

File claims and manage your account online

Most claims processed within 5 days

Free direct deposit reimbursements

Reimbursements based on your actual vet bill, not on a benefit schedule

Every customer receives a 5% discount on Pet Insurance via Farmers.com